The energy transition has already entered its next phase

The energy transition is often framed as a future consideration; a combined set of hurdles to overcome and milestones to achieve across a decades-long transformation of the global economy. However, this framing ignores the central message of the Energy Transitions panel, hosted at Foresight Capital Management’s annual investor conference in November. The panel, which featured representatives from Foresight’s private markets team as well as senior representatives from SSE and Boralex was unequivocal. The transition to clean energy is already the fastest energy shift that the world has ever seen.

The past decade has witnessed a combination of technology development, economic maturity and policy changes that have pushed the global energy system past an inflection point where power demand growth is occurring while fossil fuel generation falls at a global level. In 2024, clean power provided more than 40% of the world’s electricity generation1 and accounted for 92% of the year’s total power expansion2.

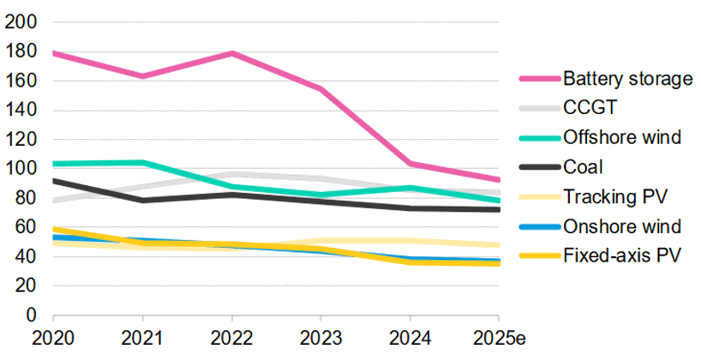

Wind or solar are now the cheapest source of new bulk electricity generation in markets accounting for 66% of global power supply3. The transition to clean energy, which was once driven by subsidies and environmental ambition, is now propelled by economic fundamentals.

The speed and direction of the clean energy transition is clear, yet the rapid rate of progress has revealed challenges that individual technological enhancements cannot resolve. To fully realise the cost advantages of very low-cost renewable power, the focus must shift towards developing an economy-wide system capable of supporting a decarbonised economy powered by intermittent clean energy.

Figure 1: $ per megawatt-hour (real 2024)4

System coordination now determines the pace of progress

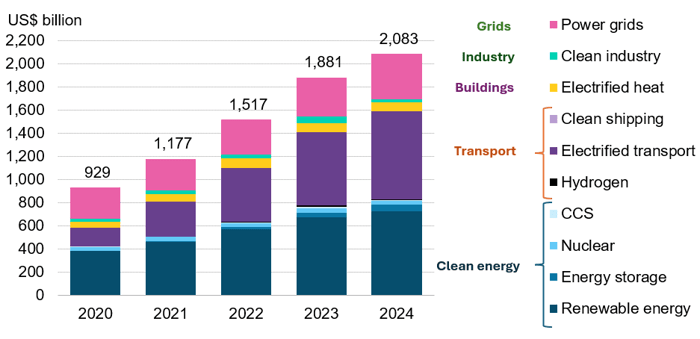

A consistent feature of the clean energy transition has been the rapid maturation of key technologies, with costs declining faster than many forecasts anticipated. Over the past five years, unit costs for solar PV and wind have fallen materially in real terms, reflecting learning effects, standardisation and supply chain maturity. This cost reduction has been accompanied by sustained increases in capital deployment across the sector, with investment in renewable energy assets rising year on year and reaching a record US$728bn in 20245.

With renewable energy generation representing an ever-increasing portion of the global power mix, the central challenge to bringing more assets online is no longer technological. Instead, constraints now sit within the wider system. More frequent periods of negative pricing, planning and permitting delays, supply-chain bottlenecks, and increasing grid congestion all highlight that system infrastructure and processes have not kept pace with the rapid expansion of clean energy.

The next stage of the transition is therefore evolving into a coordination exercise that can rapidly bring renewables online and synchronise interdependent parts of the energy system as they scale. Recent system operator modelling indicates that such a transition can also be economically beneficial, with total UK energy system costs expected to fall materially over the long term6.

Figure 2: Global energy transition investment, by sector7

Scaling the grid to enable a system built on renewables

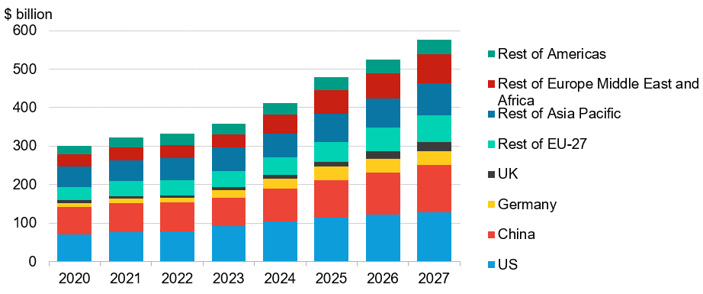

The grid will play the defining role in enabling any future system to operate at scale. With renewable assets needing to be built where resource is strongest, electricity needs to be transmitted over long distances and with great flexibility. Transmission capacity will need to expand in-line with new generation, whilst higher proportions of variable output will require networks that can move power across regions, support balancing, and integrate storage and interconnection efficiently. BloombergNEF has tracked more than $470bn of global capex into grids this year, with global spending up 16% year-on-year8.

Figure 3: Global grid investment by market9

The required grid-buildout showcases why the net zero transition is increasingly a systems challenge. The solar and wind assets underpinning the necessary energy generation may be mature and cost competitive, but their value will only be realised by a grid that is able to accommodate, transport, and coordinate their capacity at scale. Beyond enabling power flows, the expanding grid will also support greater market integration and create more stable investment conditions. Considered in full, these considerations highlight the central role that reliable infrastructure will play in supporting the clean energy transition.

Leveraging AI to run a smarter system

Amid this structural shift to a systems-based approach, AI has also begun to influence the clean energy transition in more substantive ways. Much of the public debate has centred on projections of rising electricity demand from data centres. Although AI will add to consumption, the emissions reductions it enables are expected to outweigh the increase10.

The more significant effect lies in how AI is already being applied across the system. As a general-purpose technology, AI will help accelerate the underlying system change by improving the speed, efficiency, and consistency with which new solutions are developed, and investment is directed. AI is already shortening development timelines and interpreting large volumes of technical and regulatory documentation at a pace unattainable for human teams. It is enhancing the day-to-day operation of wind, solar, storage, and hybrid portfolios, supporting more precise management of increasingly decentralised assets and helping extract greater efficiency from existing infrastructure.

As portfolios and networks grow more complex, these capabilities will become integral to coordinating the interaction between generation, storage, and the wider system. In practice therefore, AI’s contribution to the clean energy transition will not be about dramatic breakthroughs but about strengthening the underlying processes that allow a cleaner, more resilient energy system to function.

Bringing the system together

The clean energy transition is no longer defined by the search for new technologies, but by the ability to organise the ones already available into a coherent and resilient system. With a solid foundation of proven technologies and practical experience now in place, the transition has entered a phase defined by execution. The central requirement of the next decade will be to scale and coordinate the underlying system so that infrastructure, market design, and digital tools develop in a mutually reinforcing way.

1 Graham, E. and Fulghum, N. (2025) Global Electricity Review 2025. Ember. Available at: https://ember-energy.org/latest-insights/global-electricity-review-2025/

2 International Renewable Energy Agency (IRENA) 2025, Renewables in 2024: 5 Key Facts Behind a Record-Breaking Year, https://www.irena.org/News/articles/2025/Apr/Renewables-in-2024-5-Key-Facts-Behind-a-Record-Breaking-Year

3 Vasdev, A. (2025) Levelized Cost of Electricity Update 2025: Record Lows. BloombergNEF.

4 Ibid.

5 BloombergNEF (2025) Energy Transition Investment Trends 2025 [online]. Available at: https://www.bnef.com/insights/35713

6 Moore, M. (2025). UK energy costs likely to halve by 2050, says system operator. Financial Times. UK energy costs likely to halve by 2050, says system operator

7 BloombergNEF (2025) Energy Transition Investment Trends 2025.

8 BloombergNEF (2025) Grid Investment Outlook 2025. Available at: https://www.bnef.com/insights/38127/view

9 Ibid.

10 Stern, N., Romani, M., Pierfederici, R. et al. (2025) ‘Green and intelligent: the role of AI in the climate transition’, npj Climate Action, 4, p. 56. Available at: https://doi.org/10.1038/s44168-025-00252-3