The new healthcare equation: what it means for profitability, innovation and access to medicine

US profitability has long driven global pharmaceutical dynamics, but that foundation is now under pressure.

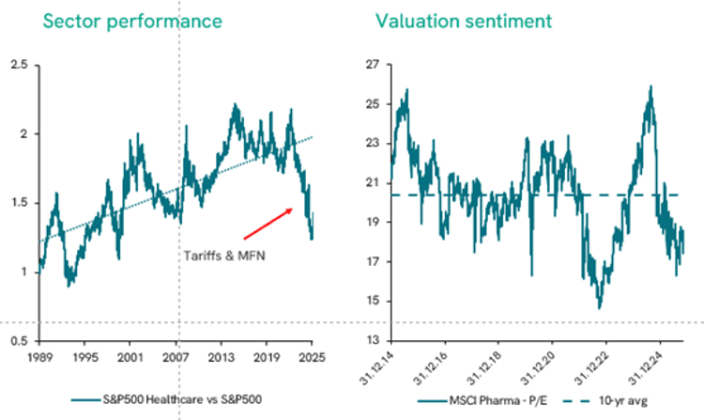

Over the past two US administrations, healthcare investors have faced unprecedented uncertainty. Drug pricing debates, trade tensions, and uncertainty in government funding have weighed heavily on the sector. This caution is visible in the market, where price-to-earnings ratios now sit well below their ten-year average.

Figure 1: The pharma sector’s P/E ratio clearly signals investor caution1

At our 2025 Annual Investor Conference in November, a panel of investors, equity analysts, and policy experts discussed policy shifts, innovation trends, and market dynamics. A clear theme emerged: the US profitability model, which has historically funded global pharmaceutical innovation and access, is under pressure. These changes are already reshaping how companies fund research, shifting priorities across the global market, and driving efficiency and innovation.

US margins are being squeezed by new tariffs, creating ripple effects.

The United States pays 2-3 times more for prescription drugs than the UK or other Organisation for Economic Co-operation and Development (OECD) peers and accounts for roughly 50-60% of global pharmaceutical sales and profits.2 High US margins have long supported Research and Development (R&D), subsidized essential but low-return medicines, and enabled operations in lower-income markets.

However, these high prices have also fuelled calls for pricing reform. Historically a Democratic issue, drug pricing has gained bipartisan attention under President Trump. The current administration has introduced tariffs linked to the Most-Favored-Nation (MFN) mechanism. These set maximum reimbursement rates for drugs available under Medicare to the lowest prices paid in a group of other high-income countries. To mitigate the large impacts of this, several companies have secured three-year exemptions, by committing to:

- Parity pricing with other key developed markets for new drug launches

- Medicaid coverage at MFN rates

- Direct-to-consumer purchase options

- Incentives for onshoring R&D and manufacturing

These agreements will reduce US margins, and companies may raise prices internationally to compensate. Nonetheless, the announcements now provide clarity that is expected to improve investor sentiment.

Impacts of the agreement will vary. Pfizer, for instance faces limited Medicaid exposure and a smaller pipeline, making it unsurprising that it was the first to sign up. Either way, the majority of other companies are also expected to sign similar agreements. Tightened margins will also have an impact beyond the big pharmaceutical companies. Smaller biotech companies and contract research organisations (CROs) ae also expected to feel the squeeze as pharma companies undertake their own research to protect their margins. Life sciences suppliers like Thermo Fisher and Danaher, both WHEB holdings, have flagged early-stage trial volume pressure but remain resilient thanks to their scale and leadership in efficiency. Other parts of the healthcare market, such as manufacturers of medical devices are expected to remain relatively insulated from drug pricing, underscoring the importance of diversification across the healthcare industry.

US margin pressure has global consequences for innovation and access to medicine.

This is not just a US story. US operating margins for blockbuster drugs, which often sit at around 40%, have historically funded essential medicines that generate little commercial return, such as antibiotics. Pharmaceutical companies also argue that these rich margins allow the companies to support initiatives in low-income countries where margins are minimal or negative. If US profitability declines, companies may reduce investment in these lower-return but socially critical areas. This is particularly worrying in a time of unprecedented cuts to global aid3. Alternatively, it may be that firms increasingly turn to emerging markets as a growth opportunity. Doing so would require significant investment in local infrastructure and a shift away from US-focused strategies.

China is already reshaping the global landscape. Once often seen as an afterthought, it is rapidly becoming a hub for clinical research. International pharmaceutical holdings such as AstraZeneca are investing heavily in China, while domestic firms are scaling rapidly.

AI and innovation are providing mechanisms to offset margin pressure and accelerate development.

As margins tighten, efficiency becomes even more critical. As FCM’s Claire Jervis outlined in her article “AI-augmented healthcare in the (dis)information age”, AI is already having meaningful impacts on the sector, fundamentally leading to more lives being saved.

Siemens Healthineers, held in the WHEB Sustainability Impact Fund, is a prime example of how leading health companies are leveraging AI. The company’s Sherlock supercomputer runs over 600 deep-learning experiments daily. One key application is in oncology, where AI automatically contours at-risk organs to safeguard them during radiation therapy. This “AutoContouring” technology replaces a highly time-intensive process traditionally carried out by physicians, while also improving accuracy. The software can now outline 47 different organs4.

In addition to delivering better healthcare outcomes, AI is also helping to reduce administrative and regulatory costs. Administrative expenses currently account for almost $1 trillion annually in healthcare spend5. Nearly 30% of the US’s excess per capita health spend compared to OECD peers comes to administrative costs6. AI tools that streamline document creation, validation, and trial approvals can shorten the eight-to-ten-year drug development cycle and free up capital for innovation, with a recent BCG model estimating R&D time and cost savings of 25-50%7. AI can also improve clinical trial design, predict potential drug interactions, reduce the risk of failure, and can even reduce reliance on animal testing.

AI will accelerate breakthrough treatments. The GLP-1 category, described by FCM’s Ben Kluftinger as “The iPhone moment for obesity treatment”, stands to benefit. AI can speed research, trials, and regulatory approval, helping companies capture what is estimated as a $100 billion opportunity. Portfolio holding Novo Nordisk is well-positioned, having cut Ozempic and Wegovy prices by 70% since launch, raising important questions about price elasticity and growth potential in a less developed direct-to-consumer market.

The US model is changing, but adaptation through AI, diversification, and international expansion is possible.

It is abundantly clear that pressure on profitability in the US pharmaceutical industry has global implications that will reshape access, innovation and wider competitive dynamics. Our view is that companies that are best able to integrate efficiency measures, diversify their revenue streams, and leverage AI to accelerate development are best positioned to survive and ultimately thrive in this new world.

1 Data from Bloomberg

2 https://www.ft.com/content/bebf2e57-42c9-4223-a317-b47390936724

3 https://www.ft.com/content/b3667445-a242-46fb-bcb3-0a21386ce355

4 https://www.nvidia.com/en-us/customer-stories/streamlining-cancer-radiation-therapy-with-ai/

5 https://jamanetwork.com/journals/jama/fullarticle/2785479 or https://academic.oup.com/healthaffairsscholar/article/1/5/qxad053/7305646

6 https://www.commonwealthfund.org/publications/issue-briefs/2023/oct/high-us-health-care-spending-where-is-it-all-going

7 https://web-assets.bcg.com/86/e5/19d29e2246c7935e179db8257dd5/unlocking-the-potential-of-ai-in-drug-discovery-vf.pdf